The investors are trying to be prepared for the Fed’s raising the interest rate in late 2015 and 2016, worried about how much it could affect the markets, but they seem to have forgotten what has been supported the markets for several years.

Have we already overcome the termination of the Feds’ QE? The answer is no. Although the interest rates are kept relatively low, and the US stocks remain near the all-time high, the markets are just supported by QEs by Bank of Japan and European Central Bank.

The portfolios of the investors of all kinds have been distorted by the QEs. According to the paper by the Fed, due to the QE the owners of Treasury securities and MBS shifted their funds into riskier assets. For example, the households sold Treasury bonds and MBS to the Fed and bought riskier assets such as corporate bonds, commercial paper and municipal debt and bonds.

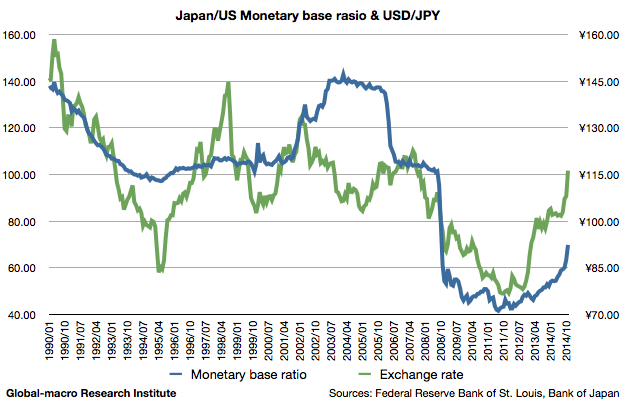

After the Bank of Japan (BoJ) decided the additional monetary easing on 31st of November, USD/JPY reached 122 once and is now traded around 120. We review if the rate is appropriate from a long-term viewpoint, after the radical depreciation from about 110.

According to Reuters (the source in Japanese), BOJ’s Kuroda said the inflation rate would remain fairly strong after the central bank achieves the inflation target of 2%. This statement is significant in the sense that he implied the moderate increasing of the inflation would be acceptable even after it becomes 2%.

As the increasing of the inflation usually follows the financial easing, considering the fact that the BOJ is willing to continue the QE until the inflation rate becomes 2%, the inflation rate is likely to increase after the QE up to around 2.5%. Consequently, the long-term interest rate, which is currently around 0.6%, couldn’t avoid to be hiked after the BOJ finishes the QE. The time to be short the bond futures is approaching.